TL;DR: Carta has forever sold itself as friction-reducing “infrastructure” for the startup ecosystem. What this recent debacle around shady secondary sales pitches reveals is that “reducing friction” often comes at a cost of over-centralizing the market. We need to think more broadly about whether keeping the startup ecosystem a bit more decentralized, even if that may seem “inefficient,” is actually a net positive in terms of trust and security for startups.

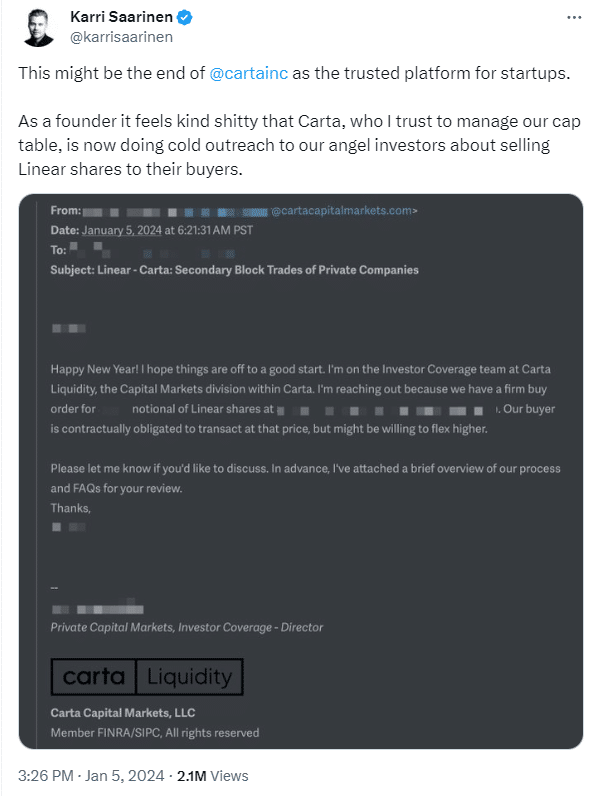

Carta, the cap table tool and self-proclaimed “infrastructure” for startup ecosystems, was all over the news recently in startup circles, because of the following:

In short, it appears that sales people for Carta’s secondary liquidity platform (for selling early startup shares to interested later-stage investors) were accessing cap table data, including investor contact info, of startups using Carta and directly pitching investors as to liquidity opportunities – all without (importantly) the knowledge of CEOs or Boards. A clever (in a mercenary sense) revenue-building strategy, but a spectacular breach of trust. No CEO or Board wants to be worrying about potential huge shifts in their cap table because their cap table software is out trying to get their angels/seed investors to sell their shares.

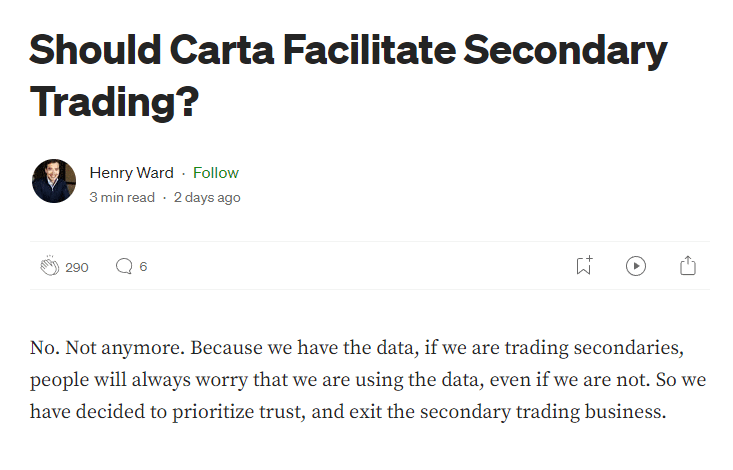

After a lot of back-and-forth, including some peculiarly aggressive accusations by its CEO, Carta eventually decided to exit the secondary market entirely; a smart move in my opinion even if it’s criticized by some as too reactive.

What I want to write about on this post is that this whole debacle reveals something concerning about Carta’s long-stated aspirations as it relates to the startup ecosystem. What does it really mean when Carta repeatedly states that it wants to become foundational “infrastructure” for startup equity, and that it seeks to reduce “friction” in startup equity markets? Being a great cap table tool – what Carta originally was – has always been an obvious positive for startups, even if Carta has repeatedly been criticized for being overpriced and too complicated and has since started receiving more heated competition from leaner alternatives; particularly Pulley.

But should founders, VCs, and other startup ecosystem players actually want a centralizing tool to maximally unify the ecosystem and reduce so-called “friction,” as Carta has repeatedly pursued, or is there something about the decentralized nature of the startup market that is actually good? Is it possible that some “friction” in how the startup ecosystem functions is desirable and positive for founders and startups?

Analogies to the decentralization philosophy of crypto, and perhaps also open source software, are appropriate here. Crypto gets lambasted for all the energy that is expended in maintaining blockchains, but the regular response is that “inefficiency” is worth the added security of not having any centralized node that market participants need to trust to behave “nicely.” Friction is a price that is sometimes worth paying in high-stakes situations where trust and security are paramount.

You see similar concerns when discussing proprietary v. open source approaches to various forms of software and hardware. Yes, there is some benefit in some contexts to relying on proprietary “infrastructure” – scale economies, data aggregation, etc. – but obviously concerns about monopolistic rent extraction loom large and very often push markets toward decentralized or even open source standards.

I’ve raised my own concerns about conflicts and interest in startup ecosystems, when self-interested players with broad brands pretend to be helping founders but are in fact using their market power to effectively extract rent from the market. For example, I wrote about how YC’s Post-Money SAFE is actually a horrible instrument (economically) for many startups, and many founders don’t get advised about how to make its terms more balanced. YC has made a ton of money from pushing the Post-Money SAFE as a “standard.”

But the selling point of YC’s templates has always been “efficiency” and “reducing friction.” Again, we see a trade-off: trusting a self-interested party (in this case an influential investor) to set so-called “standards” may in some sense reduce “friction,” but the cost of that friction reduction is significantly more dilution to startup founders. Friction reduction, and trusting a centralized party to provide it, is not a free lunch. We need to assess the full costs before determining that it’s actually a good idea.

I’ve advocated for a more open source approach to startup financing templates, where we don’t pretend anything is a “standard” that shouldn’t be negotiated, but still allow for a github-like repository of well-known starting points for negotiation. This allows for some measured benefit of standardization, while maintaining decentralized adversarial players who negotiate and ensure each deal truly makes sense for the context.

I’m also an advocate for open source cap table templates. I think automated cap table tools have over-sold themselves, particularly at the earliest stages, and founders would be wise to understand that Excel is perfectly fine (and free) until perhaps Series A, or at least post-Seed.

I’ve also written about the tendency for startup law firms to flout conflicts of interest with the VC community. They’ll build deep relationships with VCs, while parlaying those relationships into representing the companies those same VCs invest in. The founders are often told that these counsel<>investor ties will “help” them – it will reduce “friction” because the lawyers know the VCs well – but it’s complete nonsense and even contradictory to the entire point behind rules around conflicts of interest in law.

You simply can’t trust lawyers to advise you properly in negotiating with a VC if that same VC regularly sends work to those same lawyers. This is why we designed Optimal to be a company-focused firm, and we regularly turn down VCs who ask to work with us. That has a cost in terms of limiting our revenue opportunities, but not unlike Carta’s decision to exit secondaries, it’s about preserving client trust. It’s a bet that the market needs and wants a player, in our case a law firm, offering trusted advocacy above what more conflicted players can provide.

All of this suggests that friction, though sometimes spoken of exclusively in negative terms, often serves a purpose. Negotiation is friction. Diligence (including of a VC’s reputation) is friction. Competition and independent review (even if redundant) is friction. Having multiple sets of advisors representing different parties instead of everyone mindlessly trusting one conflicted group is friction. Assessed holistically, sometimes friction is worth it when interests are fundamentally misaligned.

So my advice as a VC lawyer watching how this has all played out with Carta is: the outcome here is good. It’s good that the ecosystem spoke its voice, and Carta acknowledged a fundamental problem with its business model. But let’s not miss the much broader lesson here as it relates to the many other situations in which some influential ecosystem player will promise startups “less friction” in exchange for trusting them perhaps far more than they really deserve.

I like Carta as a cap table tool, even if I think it needs to simplify itself and lower costs. I am, and have been, much more deeply skeptical of Carta as centralized “infrastructure” for the entire startup ecosystem, promising all of these wonderful benefits so long as we trust it with enormous amounts of power and data. This most recent debacle (I think) shows why others should be a bit more skeptical too.