It’s been a while since I’ve written on legal tech and startup law, and given recent developments in AI, it feels like an update is in order. For context, I’m a Partner and legal CTO at Optimal, an elite boutique law firm focused on ECVC, M&A, and Tech Transactions for VC-backed startups. We’re about 20 lawyers, company-side focused, and negotiate across from all the top VCs (and lesser ones too) and the usual suspects of Bay Area and NYC-based BigLaw.

Over the past two years I’ve reviewed and/or tested a tremendous number of new AI-based legal tech products that have hit, or will soon hit, the market. The notion that the new generation of LLMs will make a material impact on the legal industry is accurate. The capabilities being released go well beyond the typical automation tools that law firms have been integrating over the past decade or so. Lawyers of all stripes are going to get a lot more productive.

However, what’s also become clear is that (predictably) shysters are coming out of the woodwork, exaggerating where this new tech is going and what can be done with it. For just one example of that, see this X thread. Given what I’ve observed over the years regarding the very short-term memory of the entrepreneurial ecosystem, I am not surprised at all that, thanks to AI, we are going to see the second, third, fourth, and on and on attempts at building the same flawed and untenable business model of some supposed new kind of law firm or legal service provider infused (somehow) so extensively with super-advanced technology that they dominate and transform the industry.

Alas, it’s just not meant to be, even if many of us tech-forward lawyers eagerly await every new tool that makes legal practice faster, smoother, more productive, etc. For those who don’t remember, Atrium was the most visible failed attempt at building the tech-driven startup law firm “of the future.” There are a lot of views out there for explaining why Atrium failed, some (in my opinion) more honest than others. I’ll summarize my views here:

A. It was controlled by a founder (Justin Kan) who, despite being extremely successful and brilliant in his own way, not only didn’t understand the real drivers of the elite legal industry – on the supply or demand side – but had no real interest in learning them. He assumed that his personal brand had enough gravitational pull to cover up impossible economics and a weak value proposition dependent on exaggerated technology capabilities.

B. Kan also assumed that his connections with Y Combinator, which funneled both cash investment and portfolio companies to Atrium, amplified his pull even further.

C. Not nearly discussed enough, Atrium’s organizational structure hid massively problematic ethical conflicts of interest that were a ticking time bomb. Company counsel, what Atrium purported to be, is supposed to help startups negotiate against VCs, serving as an equalizer for entrepreneurs and other common stockholders negotiating super high-stakes contracts and board decisions with financially misaligned elite counterparties. Yet Atrium was funded by the VC community, had VCs on its Board, and used all of those connections to funnel portfolio companies of its investors (including YC) into its client base.

In short, over-confidence and naivete, vaporware technology, and a go-to-market strategy dependent on pretending professional rules around conflicts of interest (for protecting clients) could just be hand-waived out of existence.

I could go on and on about how doomed Atrium was from the start, including how it depended on inexperienced de-skilled (read: no real partner oversight) young lawyers dreaming of VC-like payouts, and how its fixed-fee pricing model itself incentivized rushed work and not properly serving clients. But this post isn’t about Atrium; it’s about the people who are going to be using AI vaporware to try to resurrect it.

The narrative emerging today is something like “Atrium was just too early. Now, with AI, is the right time.” I’m sorry, but it’s really not. Even if the new generation of legal AI is more powerful than what Atrium was building – and it is – nothing coming down the pike of legal AI with the current generation of algorithms is going to be so transformational as to overcome all of the other flaws of the business concept.

At the low end of law, I can certainly see new legal AI creating something like a more dynamic version of LegalZoom, backed by highly de-skilled humans shuffling paper around in the background. But this wouldn’t be that transformational, because legal automation has already been eating up the bottom two quartiles of the legal industry doing work like small business law, simple divorces, estate planning, low-stakes dispute resolution, etc. It’s why the majority of law graduates today, even many from decent schools, can barely earn enough to pay their student loans. Sidenote: I think about half of law schools should just be shut down if they can’t find a way to operate at half the cost or less.

Startups even have their own LegalZoom: Clerky for the very earliest pre-seed stages, when everything can most easily be cookie-cutter. It works great in many (not all) very early-stage contexts, and many lawyers, myself included, integrate with it.

But unlike automation tools, we (VC-backed startup lawyers) play at the elite end of law, where the stakes are much higher, and the context on the ground is far more variable and complex.

The new LLM-based generation of legal AI tools are going to make elite lawyers much more productive. We already see it happening within our own firm, and it’s influencing hiring decisions, particularly on the junior side. They will make drafting, document review, research, and other lawyer work meaningfully more productive to the point of probably shrinking the footprint of elite firms, concentrating earnings further toward the top as the real “mandarins” of elite law don’t need nearly as much on-the-ground junior labor to serve clients.

But the notion that this new technology eliminates the need for those legal mandarins – the people who not only have the years of technical training, but also the personal understanding of the client and the mix of IQ/EQ to apply legal + strategic insight to unique dynamic human contexts, is preposterous.

There is simply no way to use AI (with presently attainable capabilities) to de-skill this top end of the industry such that a new organizational structure full of lower-paid “legal technicians” can actually deliver what clients want, at a quality level that doesn’t touch malpractice. This generation of AI will, as it plays out, be the equivalent of armies of tireless and supernaturally fast paralegals and junior lawyers, at a tiny fraction of what the human equivalent would cost.

Super valuable. But as anyone who has actually worked in legal (or the military) knows, even the largest and fastest infantry can be useless (even dangerous) without sufficiently smart hands-on strategic leadership. Interesting theoretical discussions on new AI algorithms point out that even if AI isn’t really “reasoning” in an abstract sense (it’s not), many lower-end white-collar workers aren’t either. I actually agree with that, even if some find it insulting (sorry).

But the elite lawyers in high-end law firms? They’re being paid to actually reason in complex high-stakes ways that no present AI breakthroughs anywhere on the horizon, in university or corporate research labs and certainly not in the market, can supplant. That being said, their work is also embedded in workflows that include numerous mundane (boring) tasks they’d gladly outsource to a diligent and reliable tool. This is why literally every single elite law firm is working on integrating AI right now.

Hardly luddites, they understand this tech is going to make their partnerships much more profitable, while improving efficiency for clients. It’s also going to make it a lot harder for junior lawyers to enter elite ranks. Such is life in the race against the machines, or perhaps better said: against the mandarins using machines.

The shysters that will be peddling AI to create pretend startup law firms and alternative legal services will be taking one of a few (predictable) strategies:

They will exaggerate the extent to which elite legal work is or can be standardized, because their unit economics can’t work without hyper standardization.

See Standardization and Flexibility in Startup Law. VC-backed tech companies going after 9, 10, and larger-figure opportunities are not coffee shops. They all operate in different competitive contexts, with different investors, different growth expectations, different team cultures, and all sorts of other contextual dynamics that influence their approach to legal and Board issues. This is why even at the earliest stages Founders CEOs talk to human lawyers.

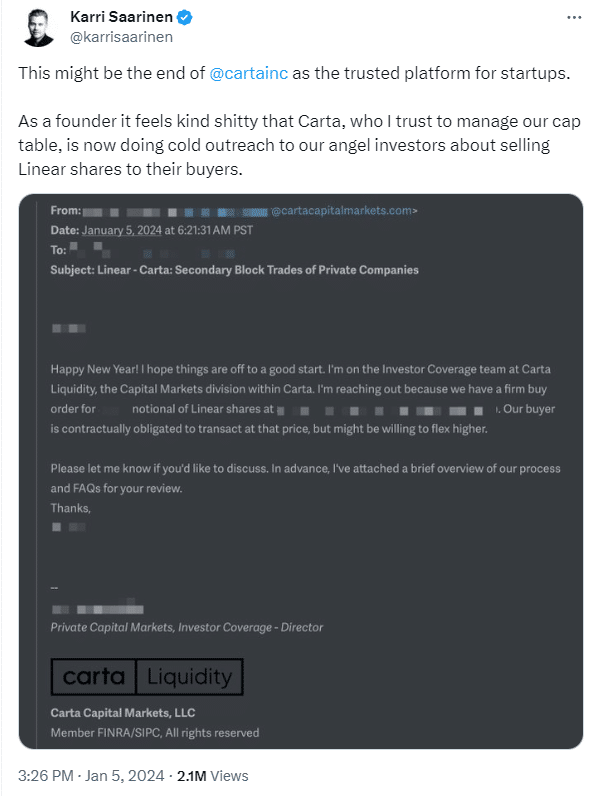

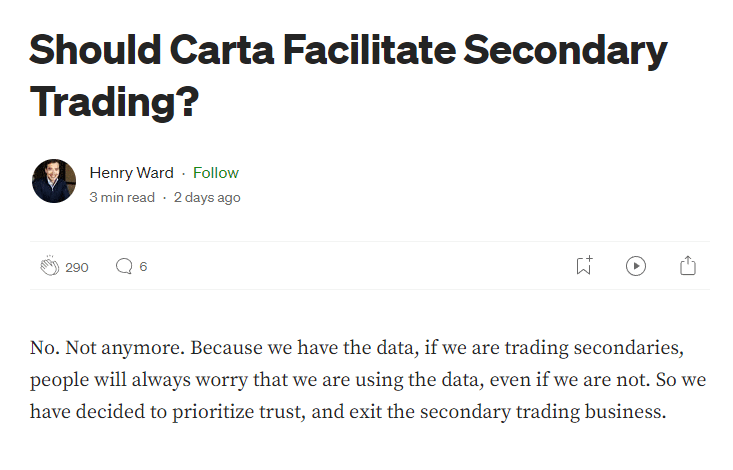

You see this play out with other automation tools that have tried (and failed) to hyper-standardize startup law: see Carta. They know their technology breaks down beyond a small level of parameters, and so they try to get clients (Founder CEOs) to believe that narrow set of parameters is all they need. But the ROI – millions – for actually negotiating contracts (flexibility) is often so high that only the most foolish entrepreneurs trust their key decisions to an automation tool.

They will de-skill their rosters in order to create margins (potentially) attractive to investors, while covering up the (significant) drop in quality.

The most expensive people at any law firm are the Partners, just as the most expensive people at a hospital are the top doctors, all for good reason. They are the ultimate quality control in a service where low quality is extremely expensive, even dangerous.

Elite law firms are built, funded, and run by a hybrid form of capital – elite Partners. They provide the financial capital, but also the extremely nuanced technical knowledge required to train and run the operation: professional human capital.

If you just layer investors, like VCs, onto this model you are not going to have a competitive advantage in the industry. Too many mouths to feed, and not enough margin. So entrants, like Atrium, rely on de-skilling – eliminating real (highly skilled) Partners, and trying to convince clients this doesn’t result in a drop in quality.

What will a drop in quality look like? Rushed (or non-existent) negotiation. Poorly thought-out legal strategy. Technical errors that even the best LLMs just aren’t algorithmically capable of catching, but now without senior expertise to correct them.

Law firms are far lower margin relative to the kinds of tech products funded by VCs. There’s no real magic to trying to create VC-like margins in professional services. It requires getting rid of a lot of the most elite talent, because that’s where the money (rightfully) goes. In healthcare, this can work at the low end (de-skilled), like nurse practitioners using tech to treat sniffles faster and cheaper than GPs. In high-end specialty care, it can be (and has at times been) disastrous.

They will be funded by, and partner with, ecosystem players who profit from a drop in the quality of legal service provided to startups.

This is exactly what happened with Atrium, which relied extensively on pushing so-called “standards” created by Y Combinator, an accelerator and VC, because YC funded Atrium, sat on its board, and pushed a lot of its portfolio companies to use Atrium. Unsurprisingly, those standards were designed to benefit investors financially, which means they cost entrepreneurs significantly, far more (orders of magnitude) than whatever they “saved” in legal fees.

This is fundamentally what so many people in the startup ecosystem misunderstand about the role of company counsel, and some even put in effort toward ensuring entrepreneurs don’t understand it. Startup Law is, at a foundational level, adversarial* and (unavoidably) zero-sum. See: Negotiation is Relationship Building. Many people want to pretend otherwise, but at the end of the day institutional investors and common stockholders see the world differently, have different goals (often), and in an exit the money can only go into one pocket or the other.

One of the most clever things I observed about how Justin Kan structured Atrium is it offered his investors a double value proposition. The first was obvious: we’ll build this supposedly massively disruptive whiz-bang-pow legal tech firm. But the second one was more subtle: send your portfolio companies our way, and we’ll ensure they negotiate the “right” way and sign the “right” contracts – meaning the ones that make more money for and give more power to… those same investors.

A brilliant move, even if profoundly illegal (it flouted rules against conflicts of interest), and ultimately not enough to overcome the bigger business model flaws. Too many smart entrepreneurs – fools can always be tricked – saw through the charade and weren’t willing to bite. I expect the same to happen with the new generation of Atriums that will be attempted in the ecosystem.

Fiction: New LLMs will disrupt the legal industry, paving the way for entirely new organizational structures taking enormous amounts of business from the old guard.

Fact: At the bottom end of the market, new legal AI will incrementally allow existing automation providers to move up-market, perhaps from the 40th percentile to something like the 50th or 60th, but nowhere near the elite firms that are most-often talked about. At the high end, everyone and their mother is working to adopt legal AI into their existing firms. Elite firms will likely be smaller and more profitable, but still very much headed by elite legal mandarins wielding more powerful productivity tech.

Post-script on Healthcare: A brief point about the new generation of AI as it applies to healthcare, perhaps the field most often compared to elite law. From my vantagepoint, I expect AI to be much more impactful in the long-run to healthcare than law, for reasons I will call (i) less competitive subjectivity and (ii) more compartmentalized service.

What I mean by less competitive subjectivity is that in healthcare the goals are more straight-forward – treat/heal the patient, and the playing field is much more standardized: biology. More straightforward goals and (relatively) uniform biological science lend themselves much more towards the implementation of algorithms and high-volume data crunching. In elite law, however, the goals are much more subjective and contextual: there are multiple players, often with their own worldviews and strategic priorities. Further, every company is very different. Different people, industries, business models, etc. EQ and human-oriented “reading the room” play a much bigger role here, and I believe that limits how far technology – in its currently developing iteration – can go in displacing humans as opposed to augmenting their productivity.

By more compartmentalized service, I mean that healthcare breaks down into much more discrete tasks that can be walled off and modularized, outsourced entirely to third-parties and technology, and then re-integrated into the patient’s treatment without a problem. Think blood labs, diagnostic testing, monitoring, pharma, etc. Elite law just doesn’t work that way for a number of reasons – largely having to do with the more contextualized and subjective nature of the work, which amplifies the friction involved in integrating third-parties lacking the full context of the “patient” (the client). This is why in healthcare I expect to see a flourishing of third-party AI-centric services woven into the market, whereas in legal far more of the development will be tools for law firms.

* When I speak of ECVC law as being “adversarial” I mean in the technical sense. It is (obviously) not to suggest overtly hostile intentions or behavior, but to acknowledge openly and honestly that there are numerous zero-sum issues on which entrepreneurs (and their employees) are misaligned with investors, and each constituency is maneuvering in order to gain an advantage. When certain players suggest that it is “no big deal” for lawyers representing companies to have close relationships with the VCs investing in those same companies, I consider that little more than a rhetorical sleight-of-hand to give investors a tremendous negotiating advantage. See Negotiation is Relationship Building.