Background Reading:

- The Best Seed Round Structure is the One that Closes

- Should Texas Founders use SAFEs in seed rounds?

Outside of Silicon Valley, Convertible Notes are the dominant form of seed round security. In SV, SAFEs are much more popular. The difference between the two effectively amounts to interest and a maturity date. For larger seed rounds, however, seed equity is another possibility.

The point of this post is not to debate the pluses and minuses of any of the above structures. The optimal one is, as mentioned in the above-linked posts, highly contextual. However, founders should understand that while SAFEs and Notes are faster and simpler to close on (usually), they come with a cost in the form of extra dilution relative to doing a seed equity round at an equivalent valuation. The math is as follows:

Dilution when raising seed as equity

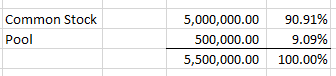

Pre-Seed Capitalization:

You want to raise a seed round with the following terms:

- Round size: $1.5 million

- Valuation (cap or pre-money if equity): $6 million

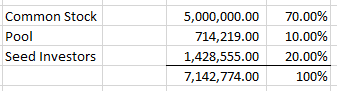

You end up doing a seed equity round, with a 10% post-money pool, but with the pool top-up added to the pre-money (as it usually is). Post-close capitalization looks like:

Key to understanding what’s going on here is how the Seed Equity price gets calculated. $6 million (valuation) / (5MM Common + 714,219 pool) = $1.05. So the seed investors paid $1.05 per share for their shares.

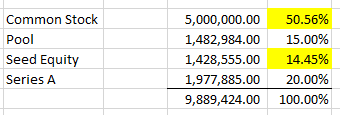

A year or two pass, and it’s time to do a Series A. The Series A economic terms are:

- Round Size: $2.5 million

- Pre-money: $10 million

- Post-Close Available Pool: 15%

After you do the deal math (explaining that is not the point of this post), the post-close cap table looks like this:

So the above is what dilution looks like after both (i) a seed equity deal of $1.5MM at a $6MM pre with a 10% post-close available pool and then (ii) a $2.5MM Series A at a $10MM pre with a 15% post-close available pool.

Dilution when raising seed as convertible notes or SAFEs

Now let’s replay the above steps, except instead of doing an equity round for the seed, let’s do a convertible note or SAFE round. We can ignore interest, which economically makes the SAFE and Note scenario exactly the same.

Pre-Seed Capitalization:

OK, now we do a $1.5 million convertible note or SAFE with a valuation cap of $6 million. Same numbers as the above seed round, except it’s structured as a convertible security instead of an equity round.

Because these are notes or SAFEs, there’s no dilution registered yet on the cap table. The dilution math is deferred until the Series A.

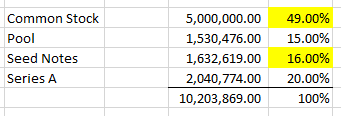

So after closing the $1.5MM, we’re now at the Series A round. Because we have notes/SAFEs, we’re required to do two calculations in this round: first we calculate the conversion price of the SAFE/Note seed round, and then we calculate the price of the Series A.

Repeating the terms of the Series A:

- Round Size: $2.5 million

- Pre-money: $10 million (VCs insist Note shares go in pre-money to keep their post-close % at 20%)

- Post-Close Available Pool: 15%

After we run through the deal math, this is what the cap table looks like:

The conversion price for the Note/SAFE is calculated by $6MM (valuation cap) / (5MM Common Stock + 1,530,476 Pool) = $0.92.

Now let’s compare the Post-close Series A cap table between the Seed Equity v. the Seed Note/SAFE scenarios.

Seed Equity –> Series A:

Seed Note/SAFE –> Series A:

What’s different? The Series A got the exact same ownership, because that’s how VC’s approach deal math. They will adjust the numbers to ensure they get their %. However, the Common Stock has 1.56% less ownership, all of which went to the Seed round. And the reason for that is straightforward, the Seed got a lower price, because the larger pool (post-A instead of just post-Seed) was built into their conversion math.

In this scenario, 1.56% is about $195K in Series A post-money terms. So the decision to do seed SAFEs/Notes instead of seed equity cost the common stock nearly $200K in Series A dollars. And that’s ignoring interest, which would put that past $200K if we’re talking convertible notes with interest. I also simplified the example by ignoring actual usage of the pool in-between rounds. A real-world example would’ve had a larger pool top-up at Series A, and therefore a larger dilution gap between seed equity and notes/SAFEs.

Conceptually the way to view this is that convertible notes/SAFEs, as currently structured, have a kind of strong anti-dilution protection built into them. And that’s apart from the more obvious anti-dilution aspect relating to valuation: that a valuation cap is just a cap, and the notes will convert at a lower price if your Series A is below the cap.

If I do a seed equity round, everything that happens to the capitalization afterward dilutes everyone, including the seed equity. There is a conventional form of (soft) anti-dilution protection (typically broad-based weighted average) in seed equity, but it is rarely triggered; only in down-round scenarios. When the Series A bargain for a larger pool and put that pool in the pre-money, the seed equity doesn’t benefit from it because their math already happened.

But in the note/SAFE scenario, the seed math is deferred to the Series A round. Anything that happens to the capitalization before that date gets built into the seed note/SAFE conversion math, so they’re protected from it. This is why the seed notes/SAFEs end up paying a lower price (92 cents) instead of the higher seed equity price ($1.05). The denominator in calculating their math is larger because of the larger pool. Lots of founders think that SAFEs/Notes only have harsh anti-dilution economics if there’s a “down round.” But that’s not entirely true. The scenario I described above was not a down-round scenario. SAFEs/Notes protect investors from dilution, much more so than seed equity, in every scenario.

If companies and investors, and in the case of SAFEs, Y Combinator, wanted to really make SAFEs and Notes more equivalent in economics to seed equity, they would allow for the capitalization, for purposes of calculating the conversion price, to be set in the security. In other words, at the time of issuing the SAFEs/Notes, we would say the capitalization is X, and that is the capitalization we will use for purposes of determining the conversion price, regardless of what the Series A negotiate for their option pool adjustment. That would not be hard to do at all. The valuation would still float and be determined at Series A, as is part of the core “deal” of a convertible security, but that full anti-dilution aspect of SAFEs/Notes would be removed.

I have rarely seen this solution actually implemented in the market. Why? I’m not sure. A lot of people aren’t even aware of this economic disconnect between SAFEs/Notes and Seed Equity, so it could just be lack of awareness. Hopefully this post helps with that. But it’s also possible that it’s just part of the “deal” that investors expect for taking convertible securities. If you ask them to move fast and take minimal protections/rights in exchange for their money, part of the price is extra dilution.

Whether or not founders think that price is fair will obviously depend on the circumstances of their company. The goal of this post was not to give an opinion on SAFEs v. Notes v. Seed Equity, because my opinion is that they are all good for different circumstances. They all have their positives and negatives. All I wanted founders to understand is that there is an economic price to using SAFEs/Notes. Make sure it’s really worth paying.