Background reading:

You only get 100% of your cap table to give away (or keep), and the sad fact is founders make all sorts of tactical errors that needlessly give up points to investors and other parties. Sometimes those errors are driven by bad advice offered by misaligned participants in the ecosystem.

One example I’ve written extensively about is the aggressive anti-dilution mechanism built into YC’s default Post-Money SAFE Template. YC portrays its template as a wonderful legal fees-saving “standard” for founders, while staying quiet about its extremely harsh economics that amplify founder dilution. YC is, at the end of the day, a VC that benefits from making founders dilute more. So be skeptical about using their templates without any modification.

The reality is SAFEs are tweaked/modified all the time, and it costs essentially nothing in legal fees to do so. In that above-linked post I offer a very simple – just a few sentences – tweak to eliminate this issue, while preserving the post-money valuation mechanism that provides transparency on how much of the cap table a SAFE is purchasing.

Another issue I wrote about over ten years ago is how founders needlessly reserve too large of an option pool at formation. They’ll just pick a number, like 20% or 10%, and reserve that amount, regardless of what they actually intend to use. They think this costs them nothing, but it’s just not true.

First, most employee new hire equity grants are made based on a % of the fully-diluted capitalization. When you offer them 2% or 3%, the denominator of that percentage includes the reserved but unused pool. It’s simple math that if you reserved too large of a pool, you are needlessly giving them more of the cap table than you otherwise would have. If you had reserved a smaller pool up-front, the 2% or 3% would be of a smaller pie, and then in expanding the pool later (which you can always do), the employee dilutes alongside everyone else.

Second, reserving too large of a pool makes it easier for VCs to argue for a needlessly large pool in your first equity round. As I wrote before:

“The pool you reserve before your first VC financing will set the baseline for negotiating how much of an option pool “top up” VCs make founders absorb.”

If your pool is at 5% going into a funding round and your VCs are negotiating for a 10% or 15% pool post-closing, it’s going to show up as a very large increase. The optics of that increase will help you in negotiation. But if you start with a 10% or 15% pool that you didn’t even need, the increase will look much smaller, which means you basically made the VC’s job easier for zero benefit to yourself.

The above two issues are not new in my writings. Stop reserving too large of a pool at formation, because it ends up giving too much equity to employee/consultant/advisor hires via equity grant calculations, and to VCs via equity round negotiations.

A somewhat newer issue that I want to emphasize here: Post-Money SAFEs make it even more costly to have an artificially large pool, given how their conversion math works. Shrink your pool to as small as possible before your SAFEs convert.

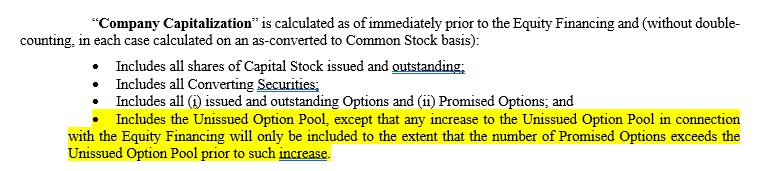

The definition of “Company Capitalization” in the Post-Money SAFE (which is the denominator for purposes of SAFE conversion) includes the pool existing before the equity round, but excludes the pool increase negotiating with your new lead VC(s).

Thus by having a pointlessly large pool at the time of SAFE conversion, you are just handing money to the SAFE holders. Shrink the pool before SAFE conversion to only exactly what you need, and the full pool increase of the equity round will NOT drop the SAFEs conversion price.

I’m not going to show specific examples of the math here. You can use the Open Startup Model (free) if you don’t have your own excel model. Suffice to say based on a few examples I’ve modeled out, you can reduce the amount of dilution your SAFE holders take, in most scenarios, by about 10% or more. Free money.

So the costs of having a pointlessly large equity pool before an equity round continue to mount:

- It means you’re giving too much equity to new hires.

- It means you’re making the job of your VCs in your equity round easier by front-loading an option pool increase they would otherwise need to argue for themselves.

- It means your SAFE holders are getting more shares from their SAFE conversion than is actually necessary.

Stop. Reserving. Stupidly. Large. Option. Pools. The emergence of AI probably means hiring needs, and associated equity pool needs, are going to shrink anyway.

At formation, reserve only what you think you will need for the next 6 months or so. And before you start negotiating an equity round, shrink your pool to cover only what has actually been used. This will save you multiple percentage points on your cap table that could be worth millions in the long-run. Again, free money. Take it.